Analysis | Decoding the Space M&A Boom: What Private Companies, Governments, and Defense Need to Know?

- Oct 29, 2025

- 5 min read

by Omkar NIKAM

For years, the space economy was a fragmented playground of startups, legacy defense giants, and national agencies all chasing orbital dominance in their own silos. But since 2024, the market has begun its most dramatic phase of consolidation, a sweeping movement of mergers, acquisitions, and strategic realignments that are redefining who controls access to orbit, data, and the space infrastructure that powers both national security and commercial innovation.

In this new era, ownership and control are no longer simply about launching satellites or operating constellations; they’re about commanding entire value chains: from launch logistics and ground networks to cloud ingestion, imagery analytics, and defense integration. The question is no longer who’s in space, but who owns space’s backbone.

1. The Great Orbital Realignment: Why Consolidation Became Inevitable

The wave of mergers and acquisitions since 2024 didn’t arise by chance. It’s a product of converging pressures, financial, strategic, and geopolitical, that are reshaping space as a fully integrated commercial-defense ecosystem.

Simply put, fragmentation became inefficient. The geopolitical tension of 2024, from escalating satellite defense projects in the U.S. and China to Europe’s scramble for launch autonomy, accelerated the logic of consolidation. Every major player realized that the real game is not about market share, but ecosystem control.

2. The New Power Brokers: Who’s Buying Whom and Why

The post-2024 consolidation map reveals a web of power transfers, not just between companies, but between entire sectors.

Satellite Operators and Earth Observation Firms

Planet Labs acquired key analytics startups to strengthen its downstream value chain in defense and climate markets.

BlackSky entered new strategic partnerships with defense primes, seeking to turn real-time imagery into operational intelligence.

ICEYE expanded its SAR constellation capabilities through strategic investment rounds backed by both commercial and government funds.

Launch and Manufacturing

Rocket Lab and Firefly Aerospace have positioned themselves as hybrid launch + spacecraft manufacturers, blending vertical integration with agile contracting for defense missions.

Arianespace, facing European launch setbacks, entered discussions with emerging space firms to co-develop reusable launch systems, a move signaling Europe’s bid to retain sovereignty amid U.S. and Chinese dominance.

Defense and Strategic Integration

L3Harris Technologies’ acquisition of Aerojet Rocketdyne and Vantor (Formerly Maxar Technologies) buyout by Advent International redefined defense-space convergence. The result? Data and propulsion, once separate segments, are now aligned under defense-grade command chains.

The U.S. Space Force and National Reconnaissance Office (NRO) are embedding these corporate consolidations into new acquisition models, where agility and interoperability are prioritized over legacy vendor silos.

3. The Strategic Logic: From Market Expansion to Orbital Control

Today’s M&A strategies are less about market share and more about influence and infrastructure sovereignty.

This transition mirrors what happened in the defense and telecom industries decades ago: once innovation outpaces policy, consolidation becomes the governance mechanism. In other words, M&A becomes regulated by market design.

4. Governments’ Hidden Hand: Strategic Endorsement of Private Consolidation

While private capital drives most M&A deals, governments are quietly orchestrating many of them.

For example, the U.S. Department of Defense’s procurement strategy now favors vendors with vertically integrated supply chains, effectively rewarding mergers that ensure end-to-end resilience. Meanwhile, Japan’s Ministry of Defense and the European Space Agency (ESA) have adopted similar postures, prioritizing partnerships with firms capable of securing national data autonomy.

In emerging economies, such as India and the UAE, consolidation is being encouraged to create national champions capable of competing globally:

India’s IN-SPACe initiative has opened the path for major tie-ups between private players and the Indian Space Research Organisation (ISRO).

The UAE Space Agency and EDGE Group have pushed local defense conglomerates toward integrating satellite and AI analytics firms to enhance their surveillance and communications capabilities.

This hybridization of public and private ecosystems means governments no longer just regulate space, they co-own the architecture through corporate proxies.

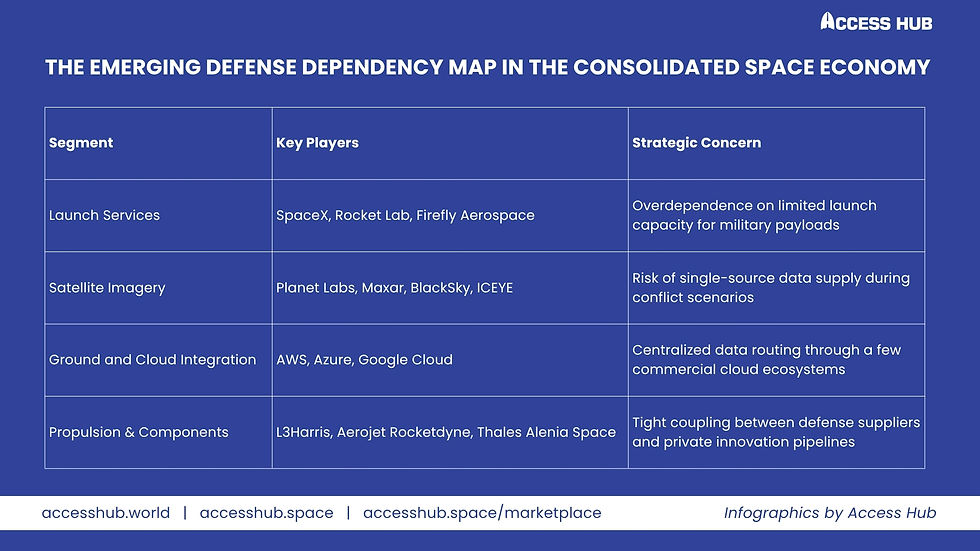

5. Defense Implications: The Fragile Backbone of Deterrence

The defense ecosystem now depends on a handful of private firms for data, propulsion, and launch capabilities. That’s both an advantage and a vulnerability.

The result is a fragile resilience, strong performance in peacetime, but potentially brittle under geopolitical stress. If a single firm faces a cyberattack, export restrictions, or bankruptcy, entire defense programs could be jeopardized.

This is why NATO and the U.S. Department of Defense are quietly mapping supply-chain dependencies to ensure “space deterrence redundancy”, a term gaining traction in policy circles to describe the creation of parallel supplier pathways across allied nations.

6. The Future of the Space M&A Cycle: Three Possible Trajectories

Looking ahead to 2026–2030, three dominant paths could emerge from this consolidation era.

The most likely outcome is a hybrid of the first two: a strategic oligopoly backed by government security interests, where control and access matter more than open competition.

7. The Consulting View: Navigating the New Orbital Power Map

From a consulting standpoint, this consolidation is not merely a market event; it’s a strategic reset.

Private Companies must understand the new ecosystem dependencies before forming partnerships or acquisitions. The right alliance can unlock government contracts; the wrong one can trap firms in closed supply chains.

Defense Organizations should map critical vulnerabilities created by overreliance on a few commercial providers. The key question is: If one vendor fails, how much national capability collapses with it?

Governments must rethink procurement, not just who delivers, but who controls the delivery ecosystem.

8. My Take: Space Is Becoming the New Industrial Base

From my vantage point, what’s unfolding in orbit is the modern equivalent of the post-war aviation-industrial consolidation of the 1950s, only faster, and far more global.

What’s different this time is that space isn’t just infrastructure; it’s governance. Whoever owns the orbital architecture effectively owns the command pathways of tomorrow’s intelligence, defense, and communications networks.

This isn’t a warning, it’s an opportunity. For those who can anticipate these mergers and alliances, the future of space isn’t just about watching satellites; it’s about designing the geopolitical architecture of access itself.

Conclusion

As the global space economy transitions from fragmentation to consolidation, the power balance in orbit is being rewritten, not just by rockets, but by spreadsheets, boardroom deals, and strategic acquisitions.

Access Hub helps organizations navigate this transformation by decoding the new M&A-driven power map of the global space economy, from identifying strategic allies to assessing supply-chain risks and competitive positioning in this rapidly converging ecosystem.

If your organization is exploring partnerships, acquisitions, or national alignment strategies in the post-2024 space economy, now is the moment to act. Because in space, as in strategy, control always begins with access.

Access Hub is your gateway to actionable intelligence and global opportunities.

Get in touch today, and let’s explore how your organization can thrive in the evolving space economy: www.accesshub.world

About Author

Omkar NIKAM, Founder & CEO, Access Hub

Omkar is a consultant, analyst, and entrepreneur with over a decade of experience advising governments, space firms, defense agencies, aerospace, maritime, and media technology companies worldwide. At Access Hub, he shapes the vision, strategy, and global partnerships, positioning the platform at the crossroads of innovation and business growth.

Comments